Trump threatens secondary sanctions on Russian oil exports, tariffs to reach as high as 100%

- Trump shortens deadline for secondary tariffs on Russian oil exports to 10–12 days

- Potential sanctions could severely disrupt global oil supplies

- OPEC+ could increase output, but market uncertainty remains high

U.S. President Donald Trump unexpectedly shortened his deadline for hitting Russia with the most severe sanctions on its oil exports to date. While the market has called the president’s bluff thus far, the sheer scale of the threat may force investors to start pricing in this meaningful tail risk.

Speaking alongside British Prime Minister Keir Starmer in Scotland on Monday, Trump said he was giving Moscow only 10 to 12 days to reach a deal to end the war in Ukraine before he would impose so-called secondary sanctions on its oil exports, cutting short his previous 50-day timeframe set on July 14.

The sanctions would slap 100% tariffs on buyers of Russian oil, with the biggest customers being India and China.

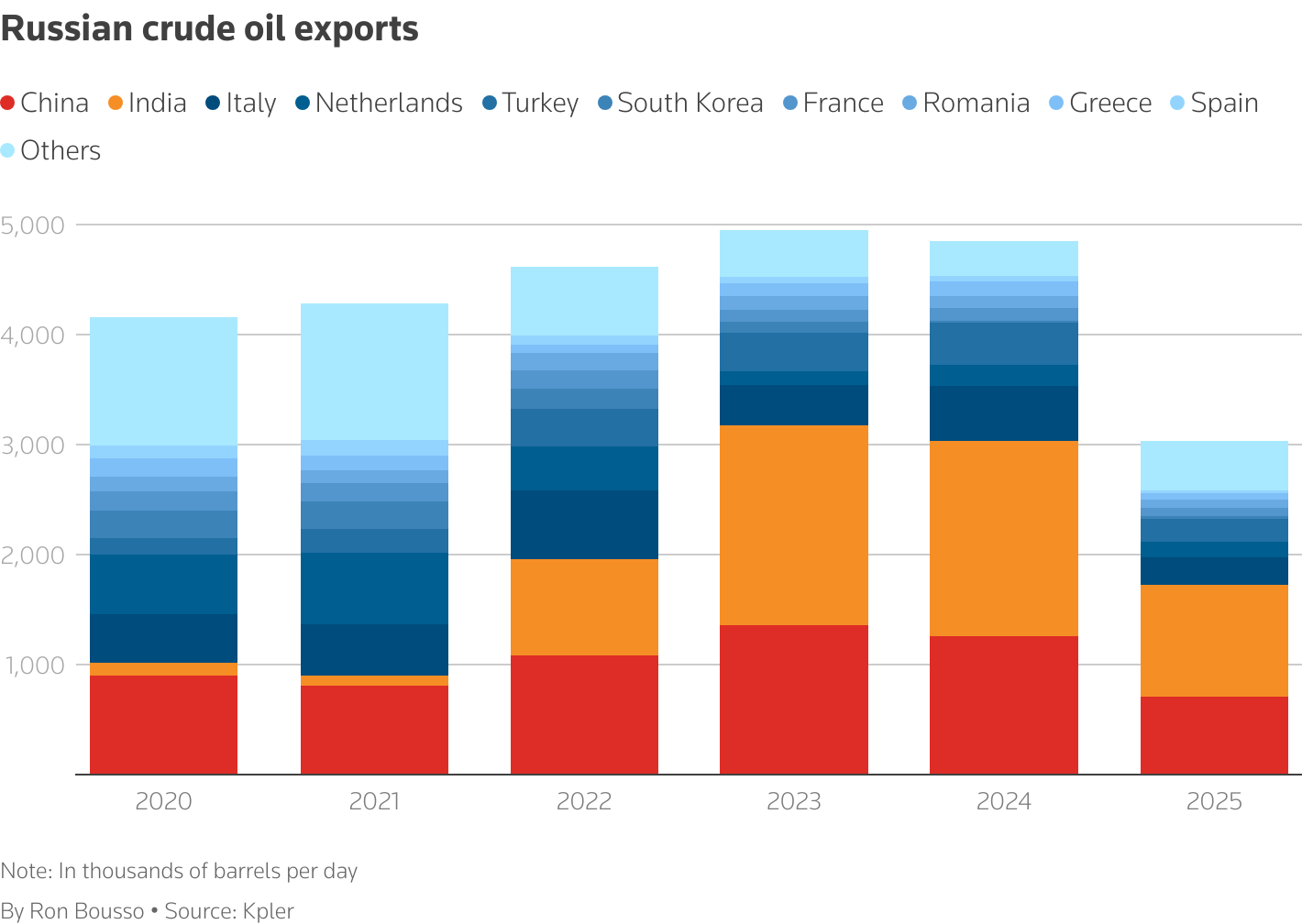

This move has the potential to disrupt global oil supplies, given that Russia exported 4.68 MMbpd of crude oil in June, around 4.5% of global demand, as well as 2.5 MMbpd of refined products, according to the International Energy Agency.

(click image to enlarge)

Will Trump actually follow through on his threat? That’s anyone’s guess. Going through with the secondary tariffs on Russia risks causing a severe spike in oil prices that could put upward pressure on U.S. inflation, an outcome that could stay Trump’s hand, even if he is “disappointed” in Russian President Vladimir Putin.

And there have been several headline-grabbing moments in recent months where the Republican president has rowed back on his threats, including the "reciprocal tariffs" originally announced on April 2 that he quickly toned down in the face of market pressure.

But Trump has also made good on some of his threats, most notably the bombing of Iran's nuclear facilities on June 22. Unlike his initial announcement on secondary tariffs, which investors appeared to shrug off, oil prices rose by nearly 3% on Monday.

So, his erratic Russia policy may make some investors wary of writing off the risk altogether.

Blunt tool. The next question is, would secondary tariffs – a relatively untested, blunt financial weapon – be effective? The answer is probably yes.

One of Russia’s key customers, India – the largest importer of seaborne Russian crude in June at 1.5 MMbpd – is currently engaged in tense trade talks with the United States. New Delhi is therefore unlikely to want to exacerbate trade tensions with Washington and thus may be apt to ditch Moscow in favor of new, though undoubtedly more expensive, energy sources.

On the other hand, China, which imported around 2 MMbpd of Russian oil in June via pipeline and by sea, is less likely to change its buying patterns since it already faces several layers of U.S. tariffs and considers its ties with Moscow to be strategic. But the Kremlin’s finances would still be squeezed regardless if India were to cease purchasing Russian oil, as China would likely be able to buy it even more cheaply.

Tit for tat. The scale of the potential new sanctions' impact on the global oil market is hard to gauge, given current supply and demand dynamics.

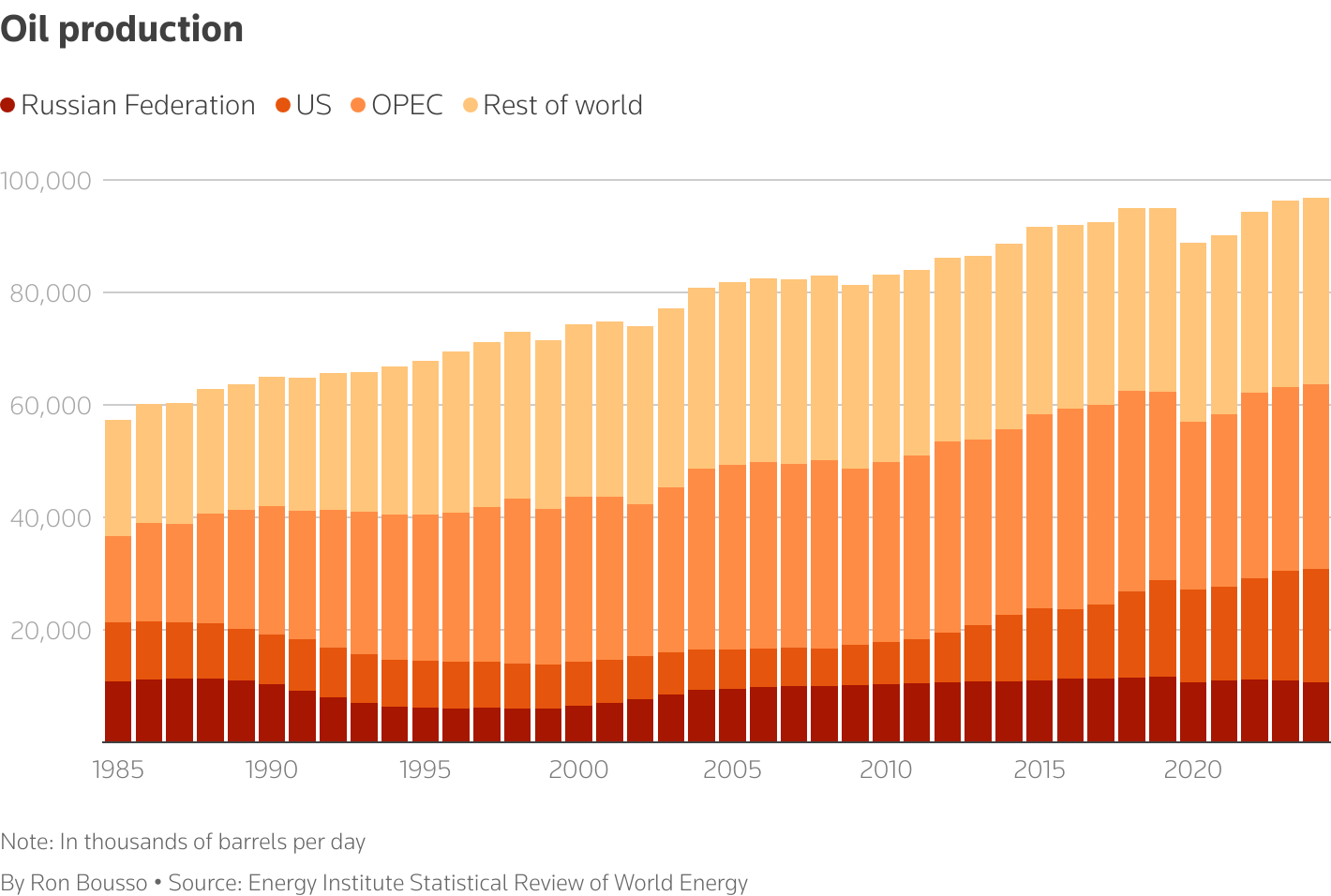

World oil demand is expected to grow by 700,000 bpd in 2025, its lowest rate since 2009, while supplies are forecast to rise sharply by 2.1 MMbpd to 105.1 MMbpd this year, according to the International Energy Agency.

The growth in supply has been driven in recent months mostly by output increases by the Saudi Arabia-led oil producing group collectively known as OPEC+. The group in April started unwinding 2.2 MMbpd of production cuts and upped the United Arab Emirates’ production quota by 300,000 bpd.

(click image to enlarge)

The OPEC+ production increases have led, naturally, to a decline in the group's spare production capacity, but Saudi still held, as of June, 2.3 MMbpd of production it can bring on stream within 90 days, while the UAE and Kuwait held 900,000 bpd and 600,000 bpd of spare capacity, respectively.

This means that the three Gulf producers could ramp up output relatively quickly in the event of a sudden supply disruption. But that knowledge is unlikely to be enough to calm markets should Trump impose his secondary sanctions, partly because of the uncertainty surrounding possible retaliatory measures by Moscow.

Revenue from oil and gas export taxes accounted for between 30% and 50% of Russia's federal budget in recent years, making these funds the single most important source of cash for the Kremlin. Putin is therefore likely to respond quite forcefully to any western measures constraining his revenue.

One such hint was given last week, when Moscow temporarily blocked foreign tankers from loading crude at Russia's main Black Sea ports following the imposition of new regulations. Loadings from the port of Novorossiisk, which account for more than 2% of global supplies, were resumed the following day, meaning Moscow was likely sending a warning that it can easily introduce similar measures.

Trump's latest threat could be an empty one, but regardless, it has shortened the fuse of a timebomb that oil markets might struggle to ignore.

The opinions expressed here are those of Ron Bousso, a columnist for Reuters.

Comments